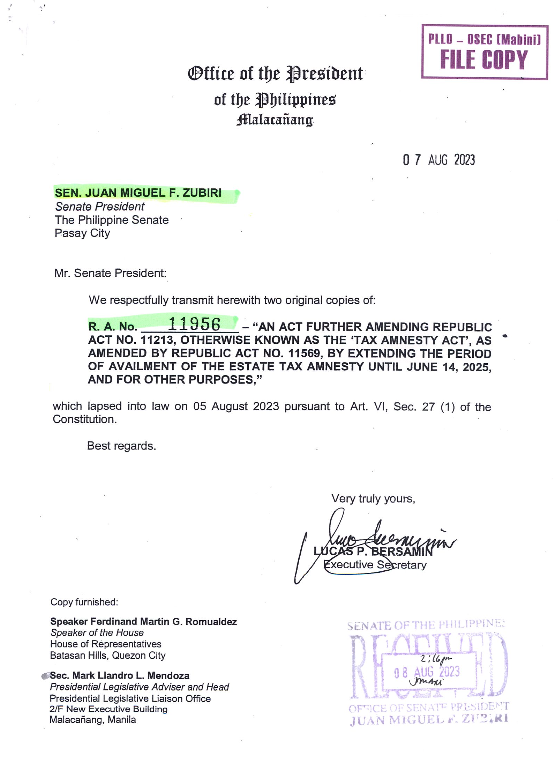

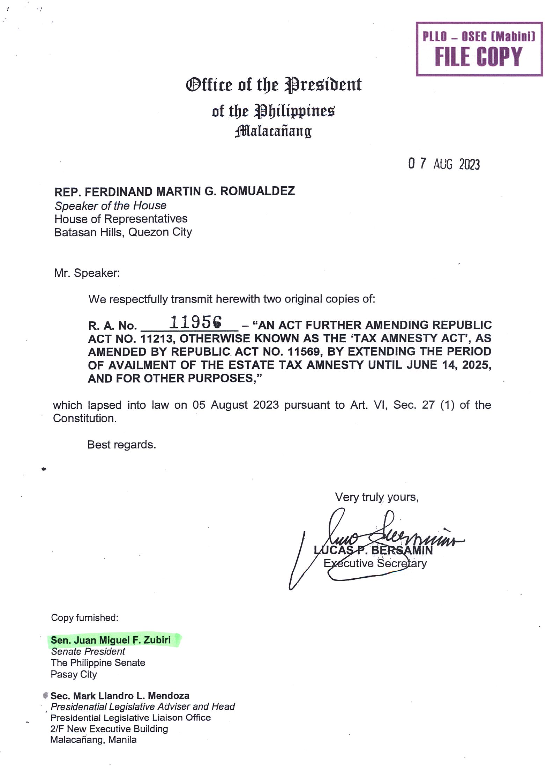

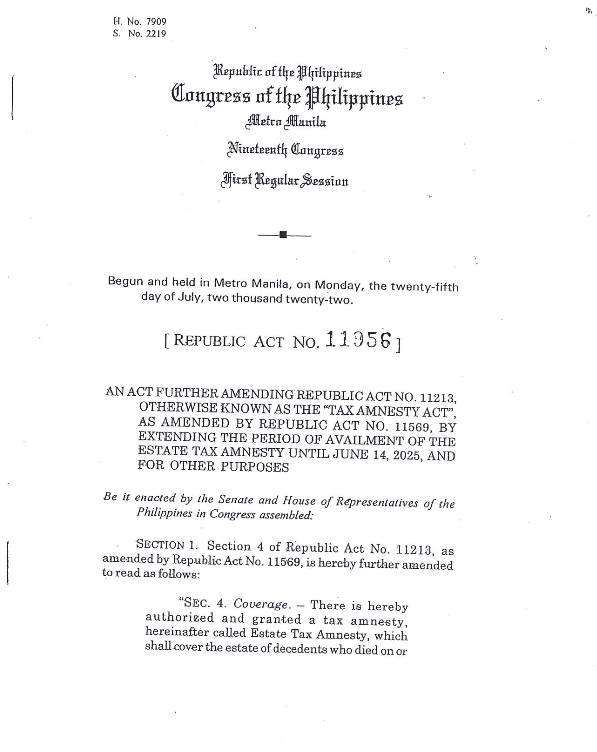

R.A. 11956 – ‘AN ACT FURTHER AMENDING REPUBLIC ACT NO. 11213, OTHERWISE KNOWN AS THE ‘TAX AMNESTY ACT’, AS AMENDED BY REPUBLIC ACT NO. 11569, BY EXTENDING THE PERIOD OF AVAILMENT OF THE ESTATE TAX AMNESTY UNTIL JUNE 14, 2025, AND FOR OTHER PURPOSES,”

“SEC. 4. Coverage. – There is hereby authorized and granted a tax amnesty, hereinafter called Estate Tax Amnesty, which shall cover the estate of decedents who died on or

before May 31, 2022, with or without assessments duly issued therefor, whose estate taxes have remained unpaid or have accrued as of May 31, 2022: Provided; however, That the Estate Tax Amnesty hereby authorized and granted shall not cover instances enumerated under Section 9 hereof.

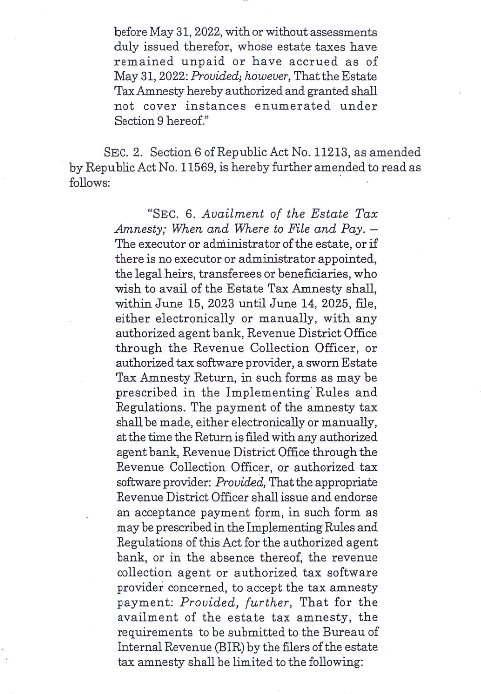

Sec. 2. Section 6 of Republic Act No. 11213, as amended by Republic Act No. 11569, is hereby further amended to read as follows:

“Sec. 6. Availment of the Estate Tax Amnesty; When and Where to File and Pay. –

The executor or administrator of the estate, or if there is no executor or administrator appointed, the legal heirs, transferees or beneficiaries, who wish to avail of the Estate Tax Amnesty shall, within June 15, 2023 until June 14, 2025, file, either electronically or manually, with any authorized agent bank, Revenue District Office through the Revenue Collection Officer, or authorized tax software provider, a sworn Estate Tax Amnesty Return, in such forms as may be prescribed in the implementing Rules and Regulations. The payment of the amnesty tax shall be made, either electronically or manually,

at the time the Return is filed with any authorized agent bank, Revenue District Office through the Revenue Collection Officer, or authorized tax software provider: Provided, That the appropriate Revenue District Officer shall issue and endorse an acceptance payment form, in such form as may be prescribed in the Implementing Rules and Regulations of this Act for the authorized agent bank, or in the absence thereof, the revenue collection agent or authorized tax software provider concerned, to accept the tax amnesty payment: Provided, further, That for the availment of the estate tax amnesty, the requirements to be submitted to the Bureau of Internal Revenue (BIR) by the filers of the estate tax amnesty shall be limited to the following:

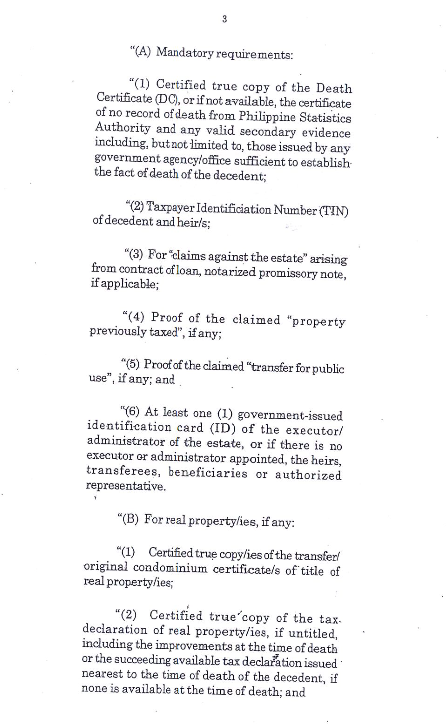

“(A) Mandatory requirements: “

(1) Certified true copy of the Death Certificate (DC), or if not available, the certificate of no record of death from Philippine Statistics Authority and any valid secondary evidence including, but limited to, those issued by any government agency/office sufficient to establish the fact of death of the decedent;

‘(2) TaxpayerIdentification Number (TIN) of decedent and heirs;

“(3) For “claims against the estate” arising from contract or loan, notarized promissory note, if applicable;

“(4) Proof of the claimed “previously taxed”, if any;

“(5) Proofofthe claimed “transfer for public use”, if any; and

‘(6) At least one (1) government-issued identification card (1D) of the executor/ administrator of the estate, or if there is no executor or administrator appointed, the heirs, transferees, beneficiaries or authorized representative.

“(B) For real properties, if any:

“(1) Certified true copy/ies of the transfer original condominium certificate/s of title of real property/ies;

“(2) Certified true copy of the tax declaration of real property/ies, if untitled, including the improvements at the time of death or the succeeding available tax declaration issued nearest to the time of death of the decedent, if none is available at the time of death; and

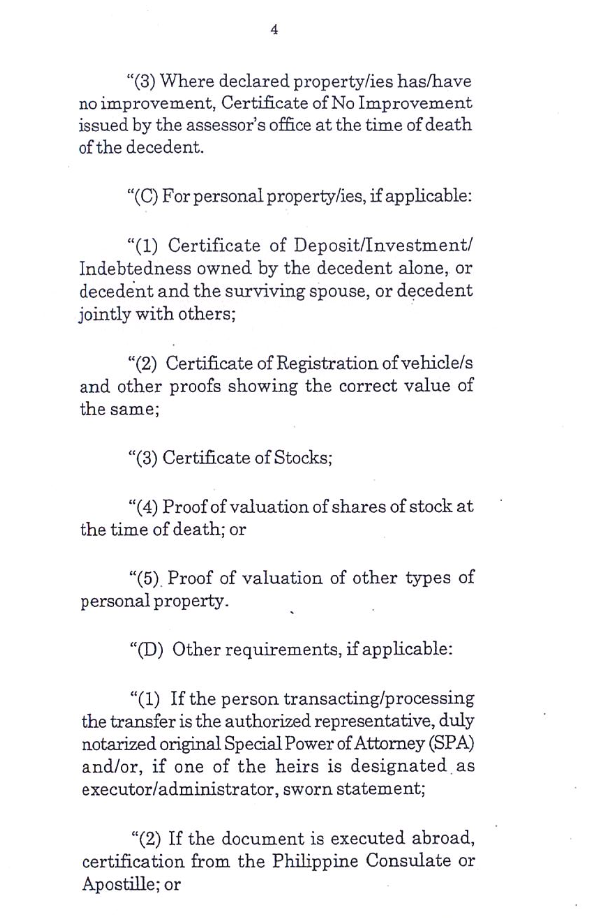

‘(3) Where declared property/ies has/have no improvement, Certificate of no Improvement

issued by the assessor’s office at the time of death of the decedent.

‘(C)For personal property/ies, if applicable:

“(1) Certificate of Deposit/Investment/Indebtedness owned by the decedent alone, or

decedent and the surviving spouse, or decedent jointly with others;

“(2) Certificate of registration of vehicle/s and other proofs showing the correct value of

the same;

“(3)Certificate of stocks;

“(4)Proof of valuation of shares of stock at the time of death; or

“(5). Proof of valuation of other types of personal property.

“(D) Other requirements, if applicable:

“(1) If the person transacting/processing the transfer is the authorized representative, duly

notarized original Special power of attorney (SPA) and/or, if one of the heirs is designated as executor/administrator, sworn statement;

“(2) If the document is executed abroad, certification from the Philippine Consulate or

Apostille; or

“(3) If zonal value cannot be readily determined from the documents submitted,

location plan-vicinity map.

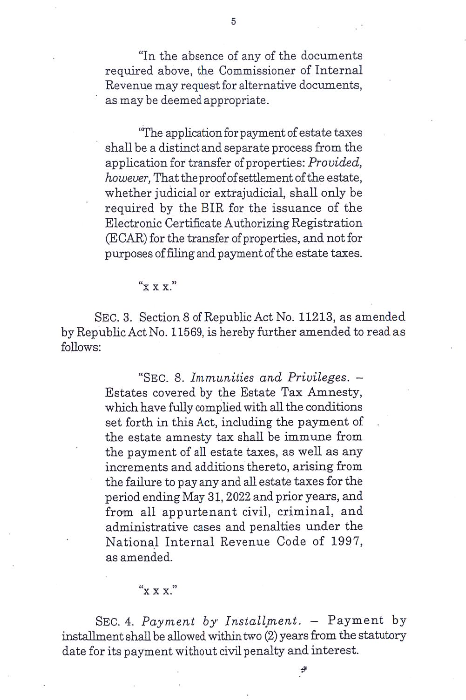

In the absence of any of the documents required above, the Commissioner of Internal

Revenue may request or alternative documents, as may be deemed appropriate.

‘The application for payment of estate taxes shall be a distinct and separate process from the application for transfer of properties: Provided, however, That the proof of settlement of the estate, whether judicial or extrajudicial, shall only be required by the BIR for the issuance of the Electronic Certificate Authorizing Registration (ECAR) for the transfer of properties, and not for purposes of filing and payment of the estate taxes.

“XXX.”

SEc. 3. Section 8 of Republic Act No. 11213, as amended by Republic Act No. 11569, is hereby further amended to read as follows.

“SEC. 8. Immunities and Privileges. Estates covered by the Estate Tax Amnesty,

which have fully complied with all the conditions set forth in this Act, including the payment of the estate amnesty tax shall be immune from the payment of all estate taxes, as well as any increments and additions thereto, arising from the failure to pay any and all estate taxes for the period ending May 31, 2022, and prior years, and

from all appurtenant civil, criminal, and administrative cases and penalties under the

National Internal Revenue Code of 1997, as amended.

“XXX.”

SEC. 4. Payment by Installment. Payment by installment shall be allowed within two y e a r s from the statutory date for its payment without civil penalty andinterest.

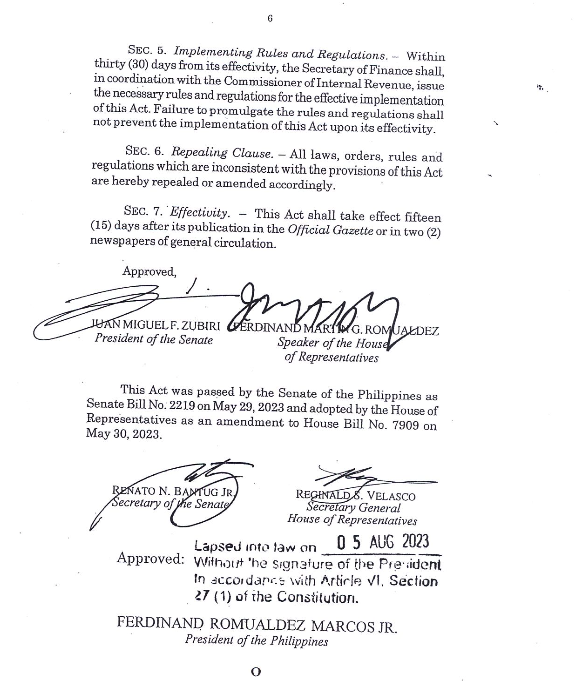

SEC. 5. Implementing Rules and Regulations. – Within thirty (30) days from its effectivity, the Secretary of Finance shall, in coordination with the Commissioner of Internal Revenue. issue the necessary rules and regulations for the effective implementation of this Act. Failure to promulgate the rules and regulations shall not prevent the implementation of this Act upon its effectivity.

SEc. 6. Repealing Clause. – Al laws, orders, rules and regulations which are inconsistent with the provisions of this Act are hereby repealed or amended accordingly.

SEC. 7. ‘Effectivity. – This Act shall take effect fifteen (15) days after its publication in the Official Gazette or in two (2) newspapers of general circulation.

Approved

JUAN MIGUEL F. ZUBIRI,

President of the Senate

FERDINAND MARTIN G. ROMUALDEZ

Speaker of the House of Representatives

This Act was passed by the Senate of the Philippines as Senate BilL No. 2219 on May 29, 2023 and adopted by the House of Representatives as an amendment to House Bill No. 7909 on May 30, 2023.

RENATO N. BANTUG JR., Secretary of the Senate

REGINALD S. VELASCO, Secretary Geneeral House of Representatives